Who Are the Dalit People and Why Is Their Story Important?

Art |

2026-05-26 11:34:30

The North America Plastic Compounding Market is witnessing significant growth, fueled by rising demand for advanced polymer materials across automotive, packaging, construction, electrical and electronics, and consumer goods sectors. Plastic compounding enables manufacturers to tailor material properties such as strength, durability, heat resistance, and appearance to meet specific application requirements. Increasing adoption of lightweight materials, growing emphasis on recyclable and sustainable plastics, and continuous innovations in polymer technologies are driving market expansion throughout North America.

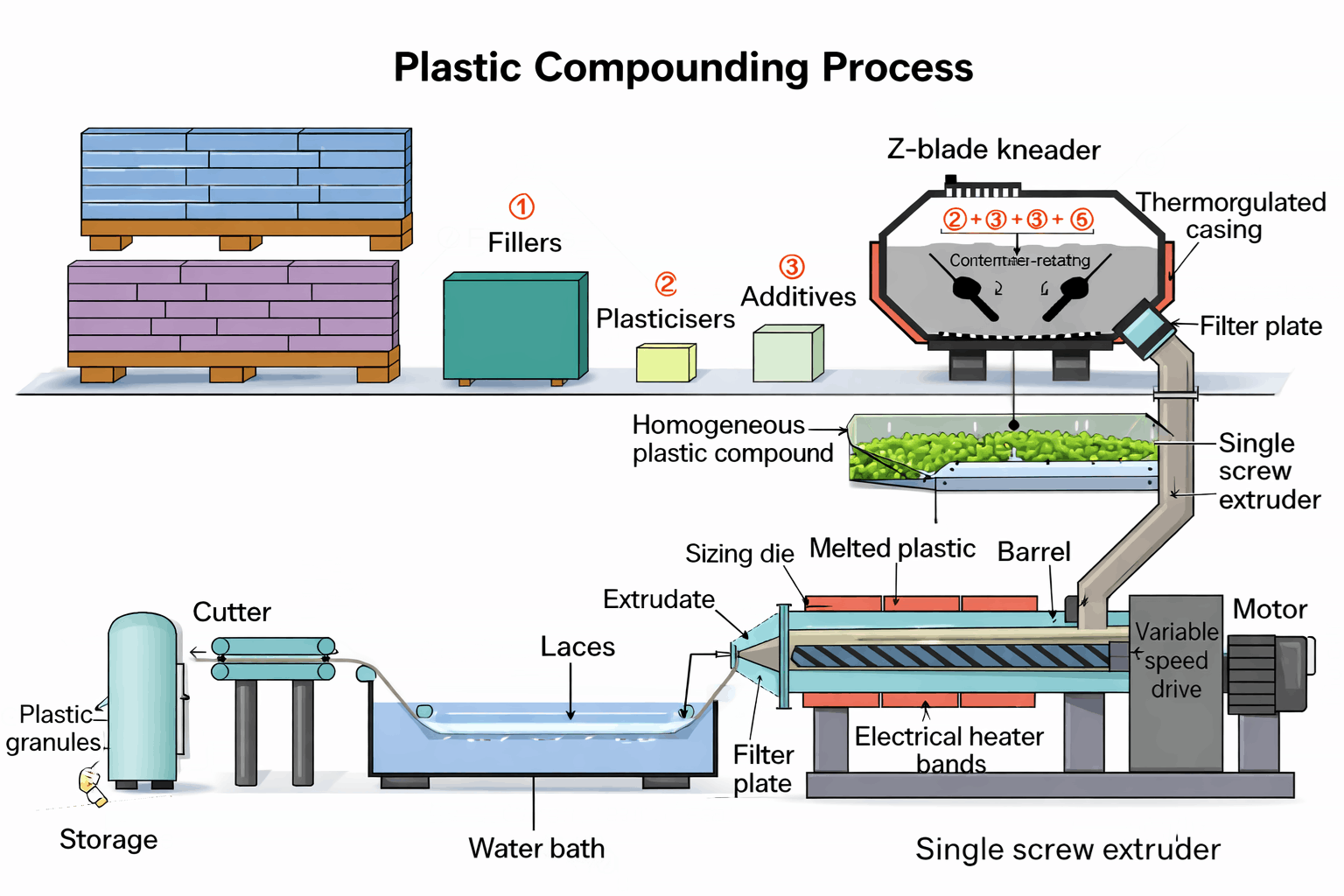

Plastics rarely go into products in their raw form. They need to be modified, blended, and enhanced before they can meet the demands of real-world applications. Plastic compounding is the process that makes this possible, and it underpins manufacturing across nearly every industry. Plastic Compounding Market Size is expected to reach US$ 142.75 Billion by 2034 from US$ 85.43 Billion in 2025. The market is anticipated to register a CAGR of 5.87% during the forecast period 2026–2034.

What Is Plastic Compounding?

Plastic compounding is the process of melting base polymer resins and blending them with additives, fillers, reinforcing agents, and other polymers to produce a compound with specific, targeted properties. The output is a customised material ready for moulding, extrusion, or film production. Properties such as flame retardancy, UV stability, colour, stiffness, impact resistance, and conductivity can all be engineered through compounding.

Request a Sample Copy of the Report: https://www.theinsightpartners.com/sample/TIPRE00007801

What Is Driving the Plastic Compounding Market?

Packaging is the single largest driver. Food, beverage, pharmaceutical, and consumer goods packaging all rely on compounded plastics. The specific properties needed for each application, from oxygen barrier performance to heat sealability and chemical resistance, are dialled in through compounding. Growth in e-commerce, food delivery, and single-serve packaging formats is pushing compounding volumes higher across PP, PE, and PET grades.

Automotive is a fast-growing end-use segment. Light weighting is a top priority for vehicle manufacturers trying to reduce fuel consumption and meet emission targets. Compounded engineering plastics replace metal in body panels, under-bonnet components, and structural inserts at a fraction of the weight. Glass-filled PP and ABS compounds are widely used in dashboards, door panels, and pillar trims. As electric vehicle production scales up, new compound formulations for battery housings, thermal management components, and high-voltage connectors are driving fresh demand.

Building and construction is another major consumption area. PVC compounds dominate this segment, used in pipes, window profiles, flooring, and cable conduit. The durability, low maintenance, and cost efficiency of compounded PVC make it the material of choice for long-life construction applications. Infrastructure investment programmes across Asia, the Middle East, and Africa are generating sustained demand for PVC compounds in water and drainage systems.

Electrical and electronics is a high-growth segment. Flame retardant compounds, conductive compounds, and high-heat-resistant grades are all critical in consumer electronics, industrial control equipment, and data infrastructure. The rollout of 5G networks, growth of smart home devices, and expansion of data centre capacity are all creating demand for advanced compound formulations with very tight performance specifications.

The shift toward engineering plastics over standard commodity grades is a structural trend running through the whole market. As product designers push for better performance in smaller, lighter packages, demand for high-value compounds with complex additive packages is growing faster than the base polymer market.

Segmentation Overview

By Type: Polypropylene holds the largest market share, driven by its versatility across packaging, automotive, and consumer goods applications. Polyethylene is the second-largest type, dominant in film, pipe, and packaging uses. PVC commands a large share in construction. ABS serve automotive and electronics applications. PET is important in packaging and fibre applications. PU and PS/EPS each serve distinct construction, packaging, and consumer goods end-uses. Other speciality polymers cover engineering and high-performance applications.

By End-User: Packaging leads by volume. Automotive and Building and Construction follow closely. Electrical and Electronics is the fastest-growing segment. Other industries, including healthcare, agriculture, and consumer goods, contribute steady incremental demand.

Key Market Players

· BASF SE

· Asahi Kasei Corporation

· Celanese Corporation

· Covestro AG

· Dow

· Kingfa Sci. and Tech. Co., Ltd.

· LyondellBasell Industries Holdings B.V.

· PolyOne (Avient Corporation)

· SABIC

· Solvay SA

Sustainability and Innovation Trends

Sustainability is the most significant force reshaping the plastic compounding industry. Recycled content integration is accelerating. Brand owners across packaging, automotive, and consumer goods sectors have set ambitious targets for post-consumer recycled content in their plastic components. Compounders are developing formulations that incorporate high levels of recycled PP, PE, and PET while meeting the same performance standards as virgin-based compounds.

Bio-based polymers are gaining ground. Bio-PE from sugarcane ethanol and bio-PET from partially bio-derived feedstocks are being compounded into sustainable grades for food packaging and consumer goods. Several major FMCG companies have specified bio-based compound grades in their packaging development pipelines for 2026 onwards.

Additive innovation is also advancing quickly. New stabiliser systems extend the service life of outdoor and automotive compounds. Reactive compatibilizers improve the mechanical performance of mixed-polymer recycled feedstocks. Nano-filler technology continues to enable property improvements at lower loading levels, reducing weight and cost simultaneously.

Buy Premium Report: https://www.theinsightpartners.com/buy/TIPRE00007801

Regional Outlook

Asia Pacific dominates the global plastic compounding market. China is the world's largest producer and consumer of compounded plastics, driven by its enormous manufacturing base across automotive, electronics, and packaging. India, Vietnam, and Indonesia are growing rapidly as manufacturing investment flows into the region. North America is a mature but high-value market, with strong demand in automotive engineering compounds, medical-grade plastics, and advanced packaging. Europe is characterised by strict regulation and strong sustainability-driven innovation. Germany, Italy, and France lead regional consumption. South and Central America show consistent growth, with Brazil and Mexico driving demand through their automotive and packaging industries.

Trending Reports:

Performance Polyolefins Market

Thermoplastic Vulcanizate (TPV) Market

About The Insight Partners

The Insight Partners is among the leading market research and consulting firms in the world. We take pride in delivering exclusive reports along with sophisticated strategic and tactical insights into the industry. Reports are generated through a combination of primary and secondary research, solely aimed at giving our clientele a knowledge-based insight into the market and domain. This is done to assist clients in making wiser business decisions. A holistic perspective in every study undertaken forms an integral part of our research methodology and makes the report unique and reliable.

Contact Us:

If you have any queries about this report or if you would like further information, please contact us:

Phone: +1-646-491-9876

E-mail: [email protected]

Also Available in: Korean | German | Japanese | French | Chinese | Italian | Spanish